Do you control your money, or does your money control you? Do you have credit card debt out the wazoo? Or do you just want to know what the heck you are spending all your money on?!?

The way to take control of your money, rather than letting it slide through your fingers, is to create a spending plan and follow it. There are several ways to do this. You need to find one that works best for you. One size does not fit all when it comes to creating a spending plan. Find one you can stick with and then DO IT!

Creating a plan

The best way to create a spending plan is to figure out what you’ve spent your money on the past 30 to 60 days and plug those numbers into one of the spreadsheet templates I will share with you in Part 2. What was that you said? You don’t have time to figure out what you’ve spent your money on the past month or two? Then make up some numbers and discover how little you really know about where your money goes and fix it later. But I highly suggest you try to use real numbers. Either way, sit down and do it NOW.

If you really, truly, have no clue then get a little notebook and keep track of every penny you spend over the next 30 days. Write down how much, where you spent it and what you spent it on.

Yearly or Occasional Expenses

Some things you pay for are not paid out every single month. These include things like auto insurance, new tires for your car, Christmas gifts, and vacations, to name a few. When the time comes to pay for these things, you want to have the money set aside to pay for them. You DO NOT want to go into more debt and put them on your credit card to be paid for later. If you put them on your credit card, you want to pay it off immediately, with no interest! So figure out what your yearly cost is likely to be for these occasional expenses and divide it by 12. Then you will know your monthly expense for them and can start to set aside money to pay for it when they come up. Don’t skip this step. Getting the brakes replaced on your car isn’t an emergency. You know it will happen at some point. Set aside the money for it, every month.

Emergency Fund

Don’t forget the importance of having an emergency fund. It’s not so you can have money to pay for those brakes, but paying for housing, food and other items if you suddenly lose your job, or if you have to have emergency surgery. Most people live paycheck to paycheck and then go into debt when an emergency pops up. Stop being one of those people. Set aside money for this, starting with $1,000. After you have your debt paid off, go back to putting money in your emergency fund. The peace of mind is worth any sacrifice to have this money in savings, untouched and waiting for true emergencies.

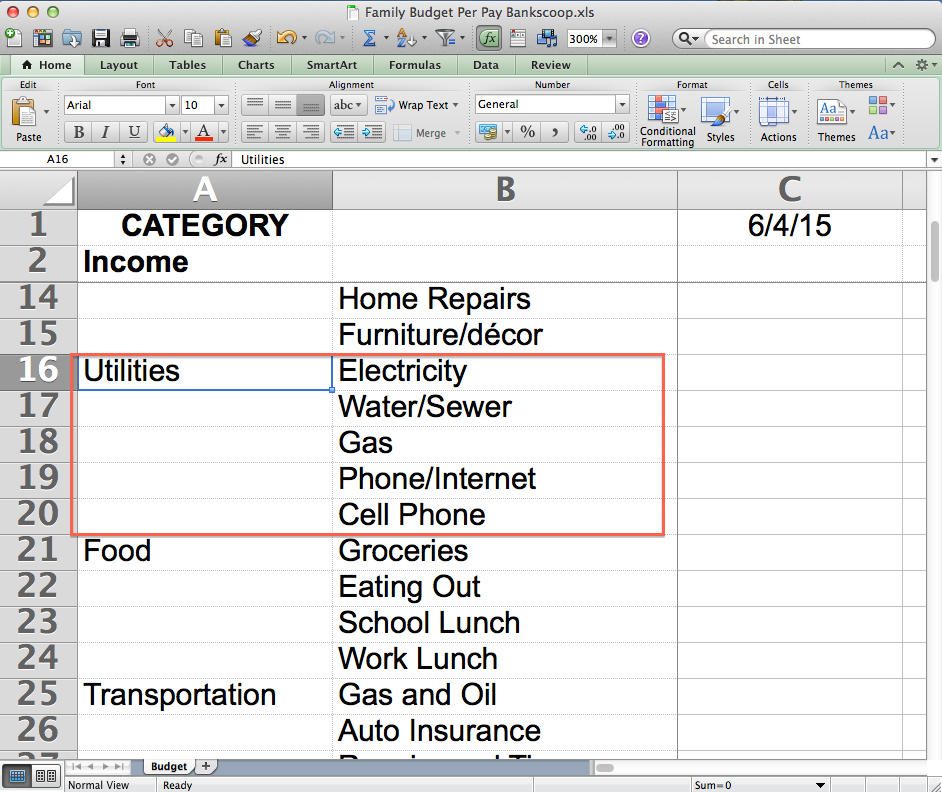

Categories

Now that you know what you are spending your money on, you need to figure out the main categories they represent, and figure out the amounts for each of these categories. Your plan can be as simple or as complex as you like. I have twelve main categories that I use, they are: Housing, Utilities, Food, Transportation, Clothing, Charitable Gifts, Savings, Personal, Lessons (piano lessons, dance lessons, etc., though it could be combined with Personal), Health, and Recreation. If you have any debt, that should be it’s own category. But within each of those categories, I have subcategories. For example, under Utilities I have listed Electricity, Gas, Water/Sewer, Phone/Internet and Cell Phone (see picture below). Each is paid to a different company, so that is why I list them separately. You can put one big amount for all of them, if that works best for you.

Now that you have divided all your expenses up by category, it’s time to put them into a spreadsheet, or somewhere that works best for you. If you don’t have all your expenses figured out yet, do that NOW. When you have it written down, then go to Part 2.

{kind=link}