In Controlling Your Money, Part 1, I discussed how to figure out where your money is going. If you haven’t done that part yet, don’t read this post until you do!

Now it is time to put it in a spreadsheet or to print out a spending plan and fill in the blanks. Below you will find some spreadsheets that I have put together for you to use. (Here are some links to sites with other budget templates you may like better: Freddie Mac Monthly Budget Worksheet, Freebie Finding Mom and Dave Ramsey).

Monthly or Per Pay Period

Next, you need to decide if a monthly plan or a per pay period plan works best for you. Because I get paid every other Thursday, per pay period is how my spending plan is set up. I tried to do monthly, but it was too confusing for me, especially in the months with three pay periods. Though, technically, my plan really is a combination of the two.

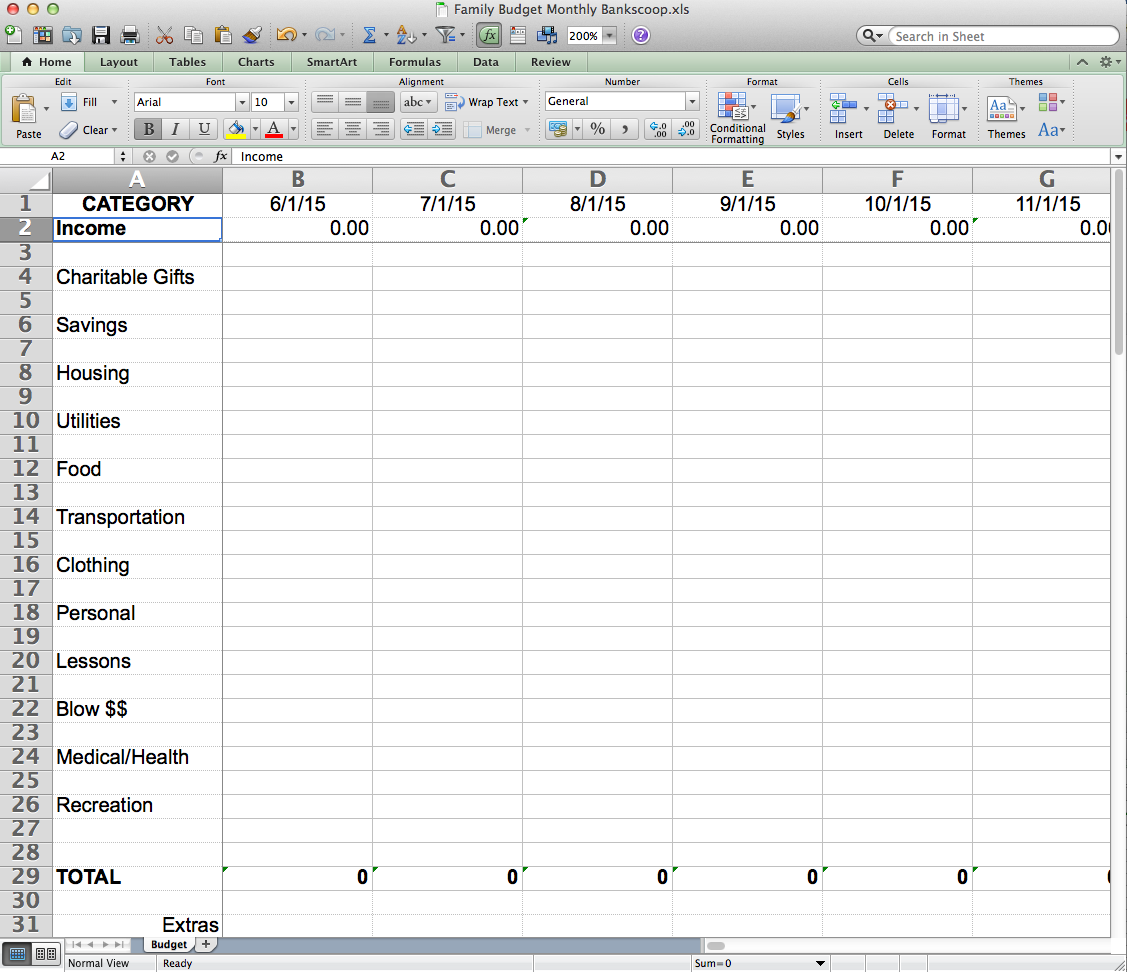

Here is an example of a simple, monthly plan:

This is how my spending plan looks:

Download the complete Excel files here:

Simple Monthly Plan and Per Pay Period Plan.

Because these are Excel Spreadsheets, you can easily change them to fit your planning needs. In the more expansive Per pay Period Spending Plan, which is set up for 26 pay periods in the year, I added a few categories that are not in the picture of my spending plan, because I no longer need them. They are: Emergency Fund to the Savings Category (mine is fully funded), and a Debt Category, with subcategories for student loans, car loan, credit cards, etc. (the only debt I now have is my mortgage.) Change the categories around to fit YOUR needs. Remember, your plan can be as simple or as complex as you desire.

Plug in your numbers

Now, plug in your numbers. The ones I told you to figure out in Part 1. Start at the top and work your way down. Put in your annual income at the bottom of the spreadsheet, in place of the fake income I put there. Then make sure the dates are correct at the top. Put them in the Excel way, i.e. =DATE(year, month, day). Next, fill in the numbers for each category. When you get to the bottom the Total should be ZERO. If it is, that means you have done it correctly. You have decided where every dollar of your money is going. If there is a balance, then pat yourself on the back! And put that extra money into building up your emergency savings or paying off debt. If it shows a negative amount, then Oops! You need to lower your planned spending in some of the categories. “But, but…I can’t! I need x amount of $$ in each and every category!” Well, guess what? YOU DON’T HAVE THE MONEY! Stop eating out so much, watch a movie at home instead of in the theater, change your thermostat so you don’t spend as much on heating or electricity, or maybe you need to rethink buying name brand clothes. Whatever you do, get the amount to $0.

And then do this for every month/pay period for the next 3 months. You can tweak it as you go along, but for now, plan where your money will go three months in advance. Me? I do a tentative plan for the next one to one and a half years, and am constantly tweaking it. You don’t have to go that far. But then again, you may want to.

Other areas in the spreadsheet

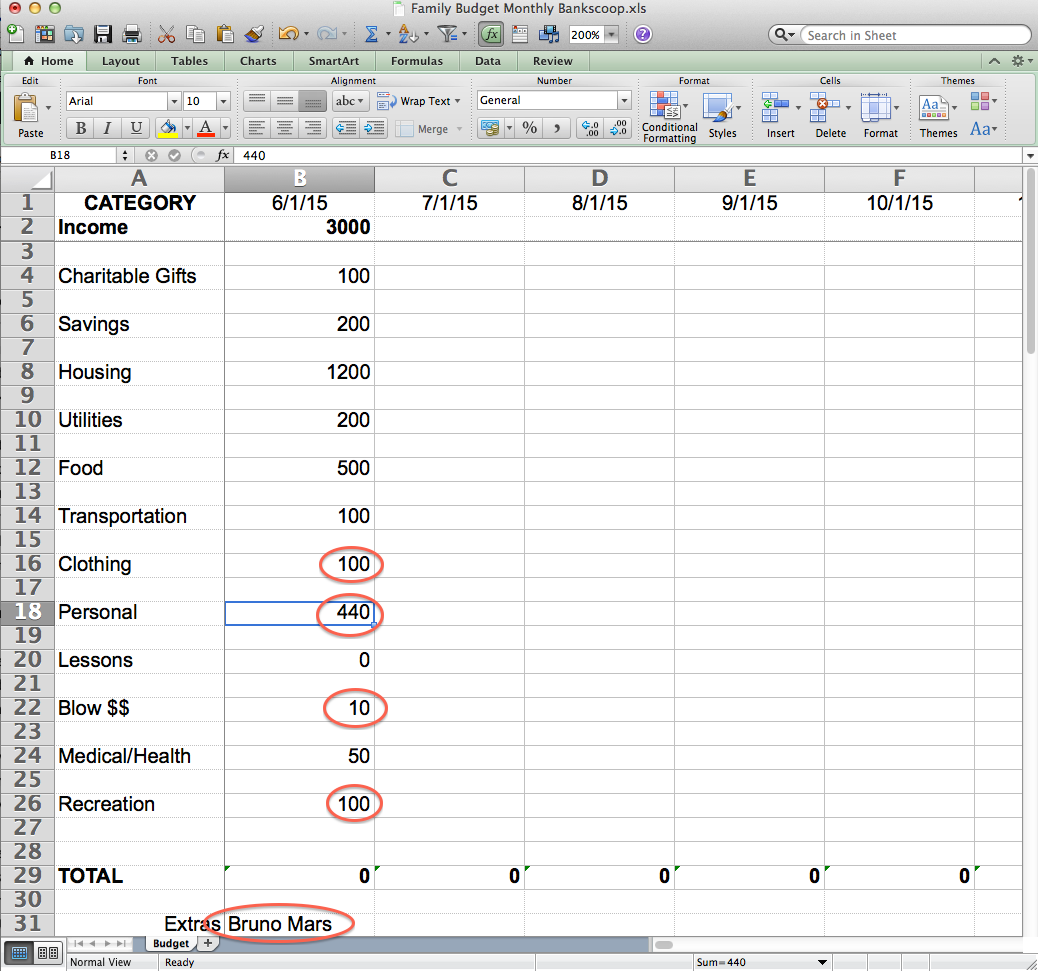

Let me explain what the other areas at the bottom of the spreadsheet are for. First “explanation of extras”. Let’s say I normally budget $15 per pay period for Entertainment. But, a Bruno Mars concert has just been announced, it’s in six months, and I want to go! I want a decent seat, and it will cost $100. Tickets go on sale in a month. So, I will add an extra $50 to Entertainment the next two pay periods to pay for the tickets. I write on the spreadsheet, under “explanation of extras”—“Bruno tickets”—to remind me that is why the amount is higher than usual, and to make sure I set aside the money specifically for that purpose. Where will the extra $50 come from each pay period? Well, I will have to spend less in some of the other categories to come up with the difference. In the example below I circled in red all the amounts I changed in order to afford the tickets. No going to the movies this month, since the whole recreation amount is going towards the ticket!

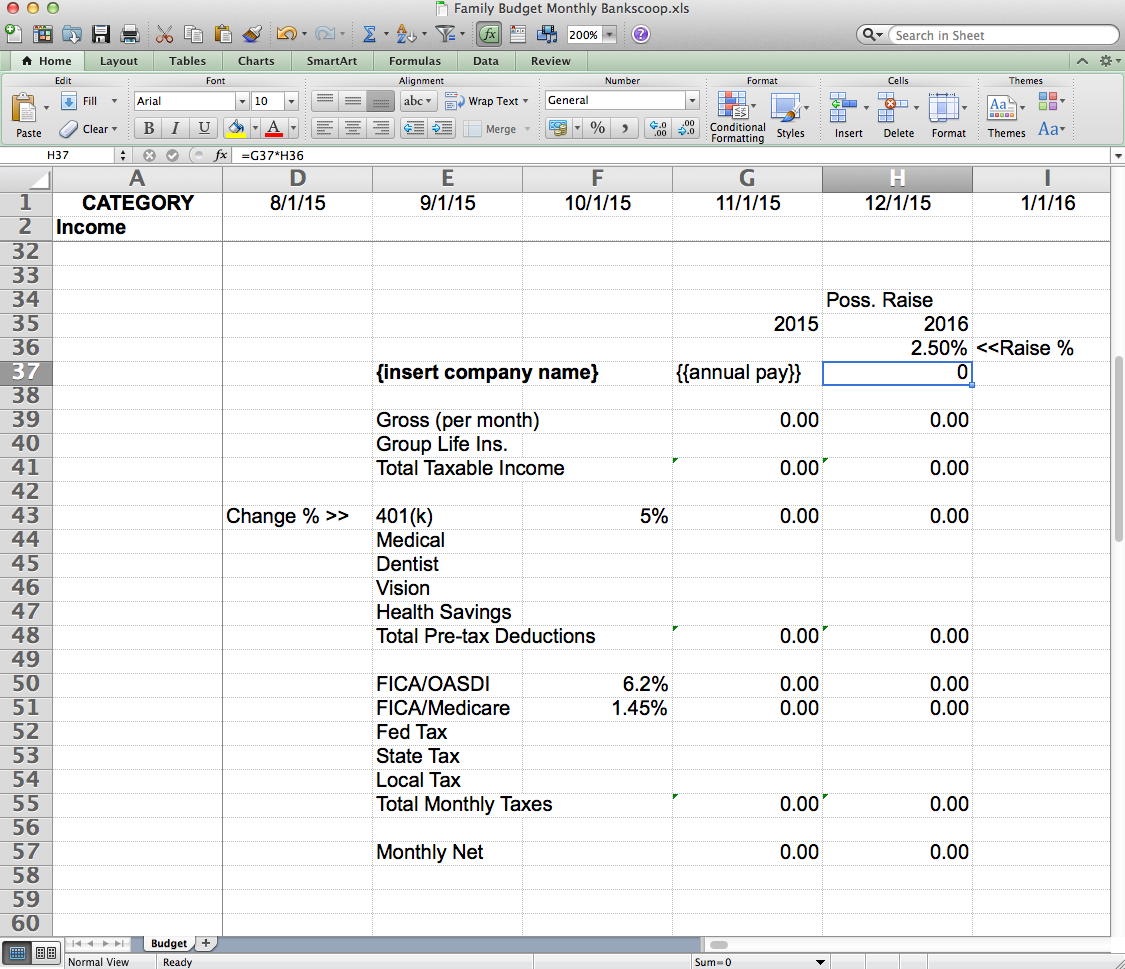

There is also the area where the breakdown is of your pay and all the deductions. This helps in planning out the future. For example, I like to make a conservative guesstimate as to what my next raise will be and plan accordingly. Or, when I find out how much my medical expenses are increasing, I put the numbers in and figure out how much less take home money I will have next year. BTW–I hate when that happens!

The included spreadsheets are set up for those in a salaried position. If you are paid by the hour you will need to change the formulas in the spreadsheet for that.

The last area is for Bonus. Again, I like to guesstimate what my bonus will be and make a plan on where that money will go. If I want to get a new couch or put it in savings, I plan for that. But add some to the “Blow” area. That means you can spend it on anything you want, without any restrictions or guilt. After all, isn’t that part of the fun of a bonus? However, if you have any debt, ALL of your bonus money should go towards paying it off.

I could go on and on in greater detail, but I think you get the concept of how to do it. Now, sit down and get going on creating your spending plan. Control your money and stop letting it control you!

{kind=link}